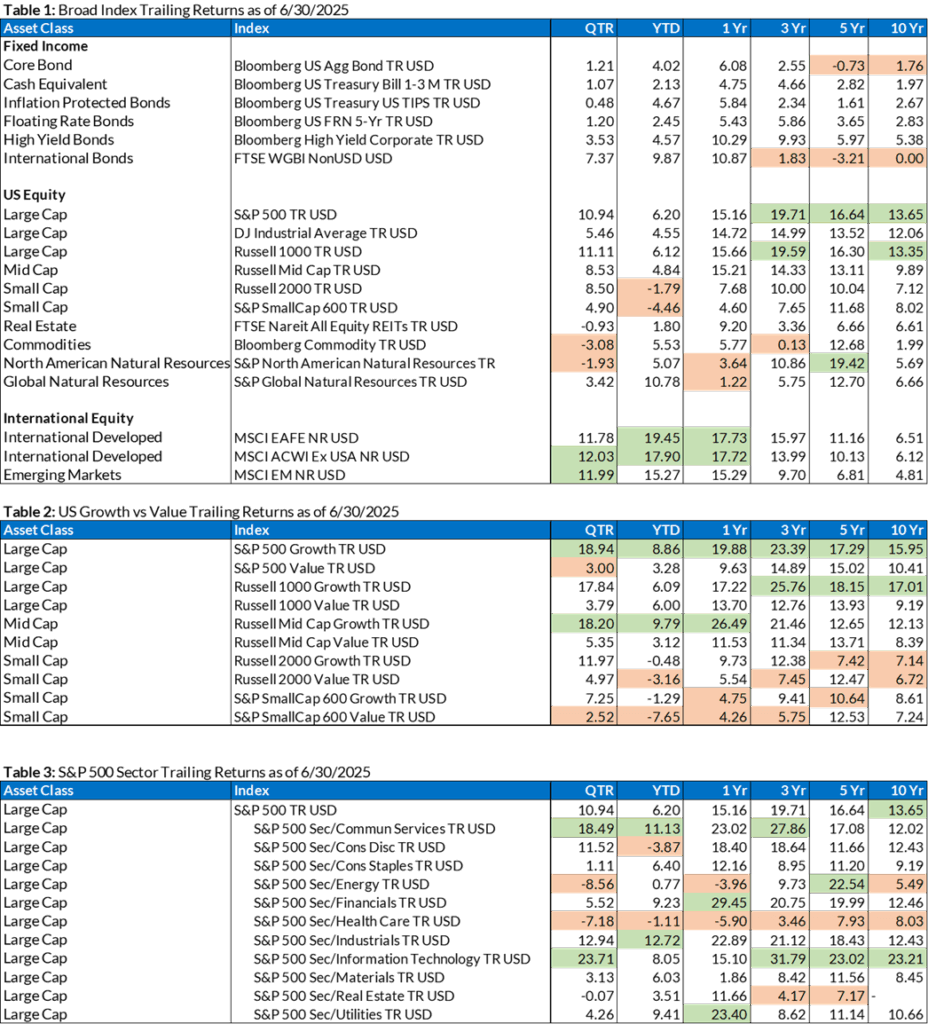

Following the sharp volatility in April, driven by tariff announcements, markets have rebounded impressively. Fueled by tech outperformance, the S&P 500 index rallied more than 24% from its April 8th bottom, finishing the first half of the year at an all-time high. The Index Trailing Returns tables at the end of this newsletter show how returns were distributed across asset classes and industries, including international stocks outperforming the US stock asset classes, highlighting why we believe it is important to hold a diversified portfolio.

Looking ahead, economic activity should likely benefit from greater policy clarity and the prospect of fiscal stimulus from the One Big Beautiful Bill. While corporate earnings are set to post solid growth, particularly within the technology sector, trade anxieties could reestablish new headwinds. Tariff deadlines set by the U.S. government are approaching and could create another round of market volatility.

Given the significant changes in U.S. tax law created by recent legislation, we have provided a summary on some of the key changes as part of the quarterly investment newsletter. The areas of the new federal tax bill — dubbed the “One Big, Beautiful Bill” — and the significant tax and financial changes are detailed below.

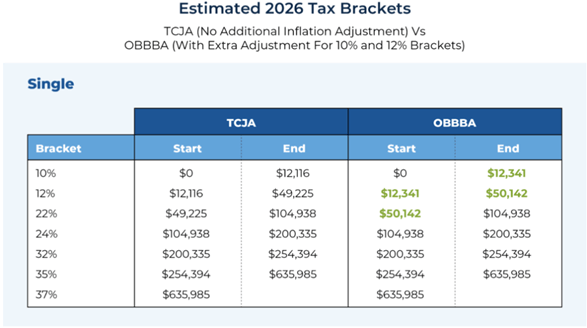

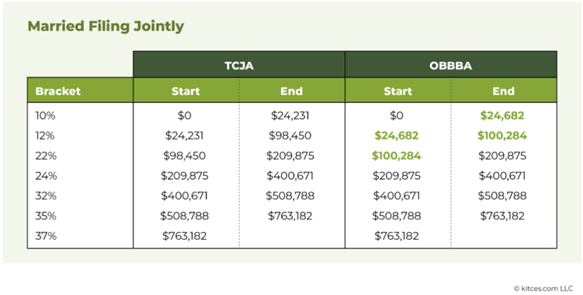

The most significant aspect of the legislation is that it makes permanent or expands many of the provisions originally introduced under the 2017 Tax Cuts and Jobs Act, which were previously set to expire after 2025. Below is a detailed look at what’s included for individual taxpayers.

Changes to Income Tax, Deductions, and Credits

Lower Income Tax Rates Extended

The individual income tax brackets introduced by the TCJA have now been made permanent. That includes the 37% top marginal rate (instead of returning to 39.6%) and lower rates across most tax brackets.

Key Takeaway: The bracket thresholds have also been adjusted upward for inflation, which may help reduce your tax liability if your earnings have remained steady. Essentially maintaining the lower tax rates and size of the brackets provides some of the biggest potential tax savings in the bill and presents the opportunity to do or make larger Roth IRA conversions.

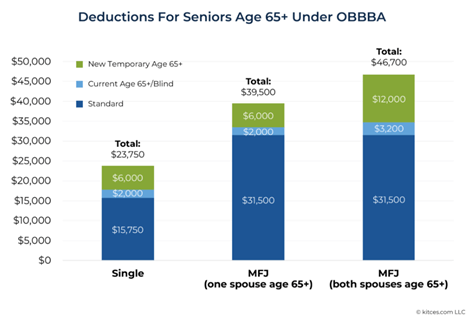

Higher Standard Deduction

The near-doubling of the standard deduction continues instead of ending after 2025. The standard deduction ($15,750 for single filers and $31,500 for married couples filing jointly in 2025) will be adjusted each year for inflation.

Key Takeaway: This may mean fewer taxpayers will end up itemizing deductions at all. For many taxpayers their total itemized deductions, such as key items of deductible taxes, mortgage interest, and charitable contributions, will not exceed the standard deduction and therefore they will not help generate tax savings. Certain strategies, such as charitable or tax bunching, could be employed in alternating years to potentially be able to itemize in certain years.

Expanded Child Tax Credit (CTC)

The CTC increases to a maximum of $2,200 per child (under age 17 by the end of the year) with a refundable amount of $1,700 in 2025, indexed for inflation in subsequent years. Starting in 2026, eligibility for the full credit amount depends on several factors: low-income families must owe at least $1,700 in federal income taxes to receive the full benefit, and the credit phase out remains the same, with the credit phasing out for individuals earning over $200,000 and married couples filing jointly earning over $400,000. A separate $500 nonrefundable credit remains for other qualifying dependents who do not meet the requirements for the CTC.

New Car Loan Interest Deduction

Starting in 2025, taxpayers may deduct up to $10,000 in interest on new auto loans, though the benefit phases out for individuals earning over $100,000 ($200,000 for married joint filers). The deduction applies only to vehicles with final assembly in the U.S. and is available through 2028. The deduction decreases by $200 for every $1,000 of income above the threshold. For example, a single filer earning $120,000 could deduct $6,000.

Key Takeaway: The IRS is expected to provide further guidance on verifying “final assembly” and a list of qualified vehicles, similar to resources for electric vehicle tax credits. Before trying to take advantage of this new tax benefit you should verify that the vehicle qualifies.

Temporary Tax Break on Tip Income

From 2025 through 2028, eligible workers can deduct up to $25,000 per year in reported tip income from their federal taxable income. The break applies to employees who receive tips subject to payroll tax withholding and earn less than $150,000 ($300,000 for joint filers).

Key Takeaway: A list of qualifying tip-based occupations will be published by the Treasury Department this fall.

No Tax on Overtime

From 2025 through 2028, eligible workers can deduct up to $12,500 ($25,000 for married filing jointly) per year for qualified overtime compensation. The break also applies to employees who receive overtime pay and earn less than $150,000 ($300,000 for joint filers).

Key Takeaway: Employers and other payors are required to file reports with the IRS (or SSA) and provide statements to taxpayers showing the total amount of qualified overtime compensation. The IRS will provide transition relief for tax year 2025 for taxpayers claiming the deduction and for employers and other payors subject to the new reporting requirements.

State and Local Tax (SALT) Deduction Cap Increased

The cap on SALT deductions was not eliminated, but it is getting a temporary boost. Beginning in 2025, the cap will rise from $10,000 to $40,000, offering potential relief to households in higher-tax states, followed by 1% annual increases to the cap in 2026 through 2029. However, the expanded deduction begins to phase out for taxpayers with incomes above $500,000. The exact benefit will vary based on filing status and household income.

Key Takeaway: For higher income taxpayers who paid more than $10,000 in combined personal property and state and local income taxes, this cap increase could be the deal breaker resulting in being able to itemize deductions and receive increased tax benefits. Additionally, there would be no SALT limitation for pass-through business entities. This means that those in one of the 36 qualifying states (such as Utah) who are paying more than $40,000 in SALT could be able to deduct the full amount if paid through their business.

Provisions for Wealth Transfer, Investments, and Retirees

Temporary “Senior Bonus” Deduction Introduced

Americans age 65 and older may qualify for a temporary $6,000 “bonus” tax deduction starting in 2025 (scheduled to run through 2028). The full amount is available to individuals with incomes of up to $75,000 ($150,000 for joint filers) and phases out for those with higher incomes.

Key Takeaway: While previous versions of the bill attempted to try and reduce taxation of Social security, nothing was passed. One key purpose of this senior bonus deduction was to provide some tax relief to those who are older and receiving Social Security benefits.

Estate and Gift Tax Exemptions Increased Permanently

The new tax law permanently raises the estate, gift, and generation-skipping transfer tax exemption from $10 million to $15 million per person (adjusted for inflation). This avoids the planned 2026 rollback and allows individuals to pass on more wealth tax-free.

Key Takeaway: This eliminates estate or gift taxes among high net worth individuals for combined lifetime gifts among annual gift exclusion and transfers at death below $15 million per person ($30 million if married). This higher exemption was made permanent which reduces uncertainty in planning.

Capital Gains Brackets Adjusted for Inflation

Capital gains tax brackets have been adjusted for inflation, allowing more investors to stay in the 0% or 15% tax range. For 2025, individuals can have up to $48,350 in taxable income, and married couples filing jointly can have up to $96,700, and still qualify for the 0% rate.

Key Takeaway: This change offers added flexibility for individuals seeking to sell appreciated assets without incurring higher tax liabilities.

Other Noteworthy Changes

Alternative Minimum Tax (AMT) Relief Made Permanent

The new law permanently extends the higher AMT exemption levels set by the 2017 tax cuts, helping more households avoid the AMT. The exemptions will continue to be adjusted for inflation, but the phaseout rate for higher earners increases from 25% to 50%, meaning the benefit tapers off more quickly for high-income taxpayers.

Major Medicaid Changes

OBBBA also includes major changes to Medicaid, including:

- Cuts of roughly $1 trillion in federal Medicaid funding over the next decade.

- Work or volunteer requirements (80 hours/month) and frequent eligibility checks for U.S. citizen recipients.

- Tighter restrictions on who qualifies for coverage and what services are included.

New “Trump Accounts” for Child Savings

In the new bill, children born in the United States between 2025 and 2028 who have a Social Security number will receive a onetime $1,000 federal deposit into a new tax-advantaged savings account, nicknamed a “Trump account.” These accounts are opened automatically once a parent files taxes and meets eligibility requirements.

Parents can contribute up to $5,000 annually, and employers may contribute up to $2,500 without it being considered taxable income. Funds will be invested in a diversified U.S. stock index fund, which will grow tax-deferred. Qualified withdrawals will be taxed as long-term capital gains.

EV and Clean Energy Tax Credits Phased Out

Several popular clean energy tax credits are set to end under the new legislation. The $7,500 credit for new electric vehicle purchases and the $4,000 credit for used EVs (both of which are subject to phaseouts if your income is too high) will expire after September 30, 2025. Tax breaks for home energy-efficiency upgrades — such as solar panels, heat pumps, and efficient windows — will terminate for property placed in service after December 31, 2025.

Key Takeaway: If you were seriously considering buying a new electric vehicle over the next year and your income is below $150k ($300k if married filing jointly) or a used electric vehicle and your income is below $75k ($150k if married filing jointly) you may want to accelerate making the purchase before September 30, 2025. Or if you were seriously considering having solar installed at your home residence you may want to consider getting a quote as soon as possible. In order to be eligible for the 30% solar credit the complete installation of the system needs to be fully installed (not just started) before the end of the year. Keep in mind that solar companies will likely be extremely busy and you also may end up paying a little more than normal given the likely increased demand.

Summary

Trade and tariff concerns still exist with deadlines approaching that could create additional market volatility due to uncertainty and potential impact on growth. Even so, international equities have outperformed U.S. equities significantly over the first half of the year. The pro-growth policies being implemented by the new legislation in the U.S., with lower tax rates, reduced regulation, and incentives to bring manufacturing back to the U.S., may spur additional domestic economic growth, much of which seems to be priced into current market expectations.

If you have any questions about how the new tax rules directly impact your situation, feel free to reach out.

Index Trailing Returns

Source: Morningstar

(Green values are the top two values in each column; the orange values are the bottom two values in each column for each table)