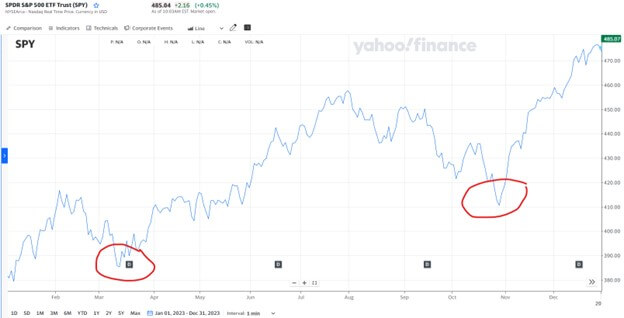

2023 was an eventful year in the U.S. financial markets with every broad index except commodities ending the year with a positive return and the S&P 500 (proxy for the US stock market) achieving a 26.29% return. As can be seen from the chart below, this did not come without some ups and downs. Both in March and October, the S&P 500 reached low points before reversing course. The last two months of the year delivered a return of nearly 16% to recover from the selloff that occurred from August through October. These ups and downs can be psychologically challenging to experience but it is part of the deal with investing in public markets. This update and outlook reviews 2023 and provides an outlook on some of the key themes to watch in 2024.

U.S. Equities

The global equity market showed strength and resilience in 2023. March and October experienced sharp pull backs, courtesy of regional bank concerns and high interest rates, respectively.

But fast forward to the end of the year, and the S&P 500 had a 2023 total return of 26.29%, the Nasdaq 100 rose by an astounding 55.1%, and the Dow Jones Industrial Average rose by 16.18%.

Likely to be a headline theme heading into 2024, there is a lot of cash on the sidelines (i.e., uninvested cash). How much is a lot? Around a record $6 trillion, according to some measures compiled by Fundstrat. That figure is more than the sum of all non-housing debt (~$4.8 trillion) held by all Americans.

This cash could help to provide equity market support in 2024 if it is invested into stocks this year. Some believe this is more likely to happen if the Federal Reserve lowers interest rates (and therefore savings rates) as expected.

Other Asset Classes

- Bonds: There was some tough sledding in this area as investors have endured a three-year bear market with the benchmark 10-year Treasury yield trading in a wide range between 3.253% to approximately 5.0% throughout the year. Bond buyers were likely feeling better once interest rates moved lower toward the end of 2023 where the Bloomberg US Agg bond index saw a 6.82% increase the last quarter.

- Gold: GLD (SPDR Gold Trust ETF) had a resilient and impressive year, rising 12.69% in 2023, even as interest rates rose for the majority of the year. Spot gold prices breached all-time highs in early December 2023 and pulled back to end the year. Precious metals could garner more attention this year, with interest rates expected to stay steady to lower.

Inflation

Commodity Prices: Broadly measuring commodity prices using the S&P Goldman Sachs Commodity Index, the index fell in 2023, indicating lower wholesale prices across a broad range of commodities. Ideally, this trickles down to the consumer if companies do not mark things up too much.

Consumer Price Index (CPI): Government data showed that consumer inflation, as measured by the Consumer Price Index, peaked year-over-year in June of 2022 at 9.1% and declined steadily throughout 2023. However, it may not feel like it when you purchase goods and services. “Stuff” is still expensive, with service pricing and shelter pricing remaining stubborn. Core CPI (which excludes volatile food and energy) showed a rise of 4% year-over-year, according to the last release in 2023 of November data.

Core Personal Consumption Expenditures (PCE): The Fed’s most recent forecast shows its favorite inflation gauge, Core PCE, falling to 2.4% in 2024, 2.2% in 2025 — and ultimately reaching their target of 2% in 2026.

The Consumer Heading Into 2024

How has the U.S. consumer remained so healthy with everything they have battled against?

Consumer Confidence: Consumer confidence increased in unison with the direction of the stock market rally in November and December, indicating higher levels of consumer optimism. The final reading in 2023 showed consumer confidence at a five-month high.

Consumer Debt: While consumer confidence is trending higher, so is consumer debt. Consulting the Federal Reserve Bank of New York, we see a rising uptrend as of the last data release for Q3 2023, with non-housing debt at $4.8 trillion. Of this amount, total consumer credit card debt has surpassed 1 trillion. With elevated credit card interest rates, it is no picnic for indebted borrowers. Yet, consumers keep spending, and the trend has been spending on experiences versus material goods.

Prospects for lower interest rates in 2024 could help reduce the impact of borrowing or fuel this narrative and embolden the already willing and able U.S. consumer.

Retail Sales: Monthly retail sales results exceeded estimates from August through December, further fueling the resilient consumer theme.

We saw a mostly steady uptrend of retail sales throughout 2023. Let’s keep in mind that retail sales figures are not inflation-adjusted, so depending on who you ask, the indicated strength is debatable.

The post-Covid consumer spending has been impressive. However, early data available for the holiday shopping season did show some evidence of a possible slowdown, with the holiday shopping season data coming in at a 3.1% year-over-year gain versus the 3.7% expected.

There has to be a breaking point in consumer spending, right? Well, many thought this over the last couple of years, and they have been proven wrong. We will see what 2024 brings.

Labor Market

Some would call 2023’s labor market the best on record — with good reason. Low unemployment and narrowing wage inequality, among other factors, have contributed to the positivity.

Jobs growth was white-hot through the middle of 2023 before cooling somewhat. The cooling has been viewed as constructive and even goldilocks-like when considering the November and October jobs data.

Looking ahead, economists offer varying perspectives on 2024’s labor market, with the consensus calling for stability in job growth. Further cooling in inflation as well as a calmer and more accommodating Fed play into this expectation.

Of course, there are two sides to every coin, and other analysts have other opinions.

Energy

After markets saw rising crude oil in the first half of the year, the narrative shifted directions, with crude oil and gasoline prices falling in the final two months of 2023. In fact, Crude Oil (West Texas Intermediate) finished 2023 more than 10% lower than where it began the year. Lower gas prices at the pump for most of America certainly is helpful.

Heading into 2024, reports of electric vehicle (EV) sales slowing down are in the headlines. Longer days on the lot until sales and growing inventories are the themes for now, and manufacturers have begun to cut back on production. Talk of renewable energy supply chain bottlenecks is also in the news.

It’s also an election year, and that may have some influence on pump prices. “There’s a really strong inverse relationship between pump prices and approval ratings at a presidential level, and it hasn’t changed in four decades,” Clearview Energy Partners Managing Director Kevin Book said.

Election Year

On the note of the presidential election, associated volatility could find its way into markets. However, according to U.S. News, the S&P 500 has yielded an average 7% return in election years dating back to 1952.

The election cycle could add more headlines to a market, with investors weighing the economic policy of the potential presidential winners.

Federal Reserve Outlook

As major U.S. market indexes rose impressively in November and December, so did expectations for Federal Reserve (Fed) rate cuts. High hopes surrounded Fed rate cuts, but there was some disparity between the Fed’s commentary and the market’s pricing at year’s end.

At the end of 2023, market expectations were for cuts to begin in March of 2024, with a total of six to seven quarter-point rate cuts priced in, according to the CME FedWatch Tool (CME FedWatch Tool, 2023). Yet, the Fed has broadcasted a message of three cuts in 2024.

In fact, while Fed members see rate cuts as likely in 2024, the path remains highly uncertain, according to the December meeting minutes released on January 3rd.

Fed officials were optimistic about the path of inflation in the meeting minutes, but market bulls who expected a super-dovish-sounding Fed ready to cut rates quickly and rapidly were left somewhat disappointed.

Perhaps we have indeed seen a market that has gotten a bit ahead of itself on rate-cut hopes. On the day of the Fed meeting minutes release, markets were still pricing in the first rate cut of 2024 to occur in March to the tune of a 66.5% probability of a quarter-point cut at the March 20th meeting.

Long-Term Effects

As always, we will keep you apprised of what we know when we know it, with a focus on how what happens in the news and in the markets impacts your investments.

However, we encourage you as a long-term investor to keep in mind the markets of March 2020, and more recently, March and October 2023, when world events led to dips. Selling assets in a panic during Covid days, regional bank pressures, or times of rapidly rising interest rates has proven to be the wrong choice each time

In its 66-year history, the S&P 500 has delivered positive annual gains roughly 70% of the time. That’s not to say that the bumps in the road don’t deliver brutal news headlines and trigger emotions — but historically, remaining level-headed and disciplined puts the odds in your favor.

This helps us keep in mind the benefits of long-term investing as we head into a new year. And, of course, if there is anything on your mind regarding stocks, interest rates, energy, or your portfolio, please feel free to reach out. We are always here as a resource for you.

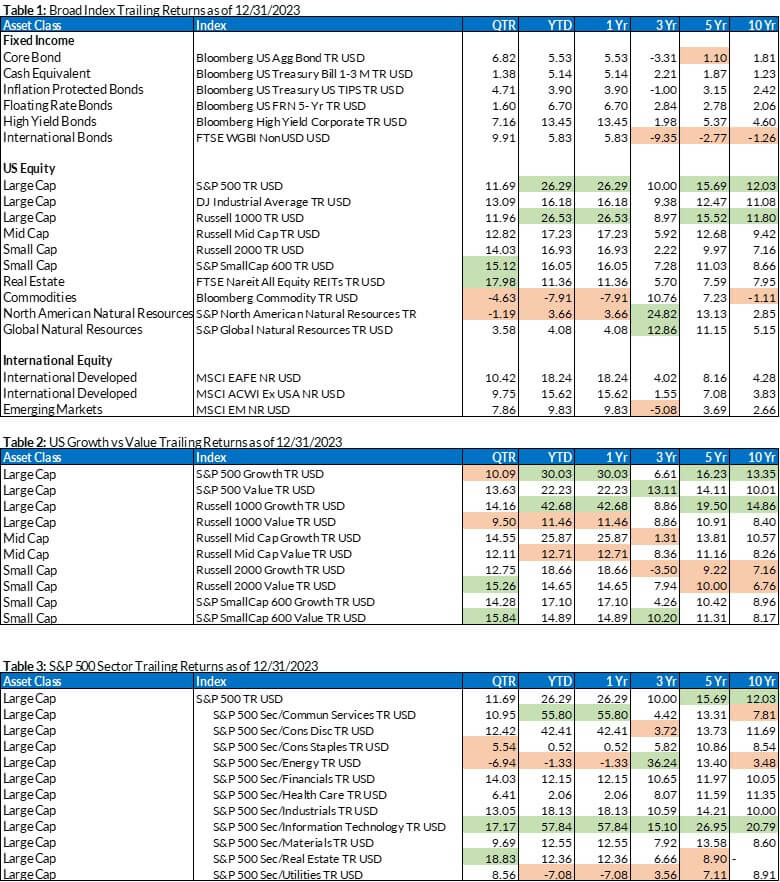

Index Trailing Returns

Source: Morningstar

(Green values are the top two values in each column; the orange values are the bottom two values in each column for each table)